FCA Consumer Duty changes for our partners

The FCA Consumer Duty sets higher and clearer standards of consumer protection across financial services. As of July 2023, new rules will be implemented that are likely to apply to customers our partners do business with, in their capacity as an FCA authorised firm. We support the principle of the duty and aim to deliver good outcomes for all our customers.

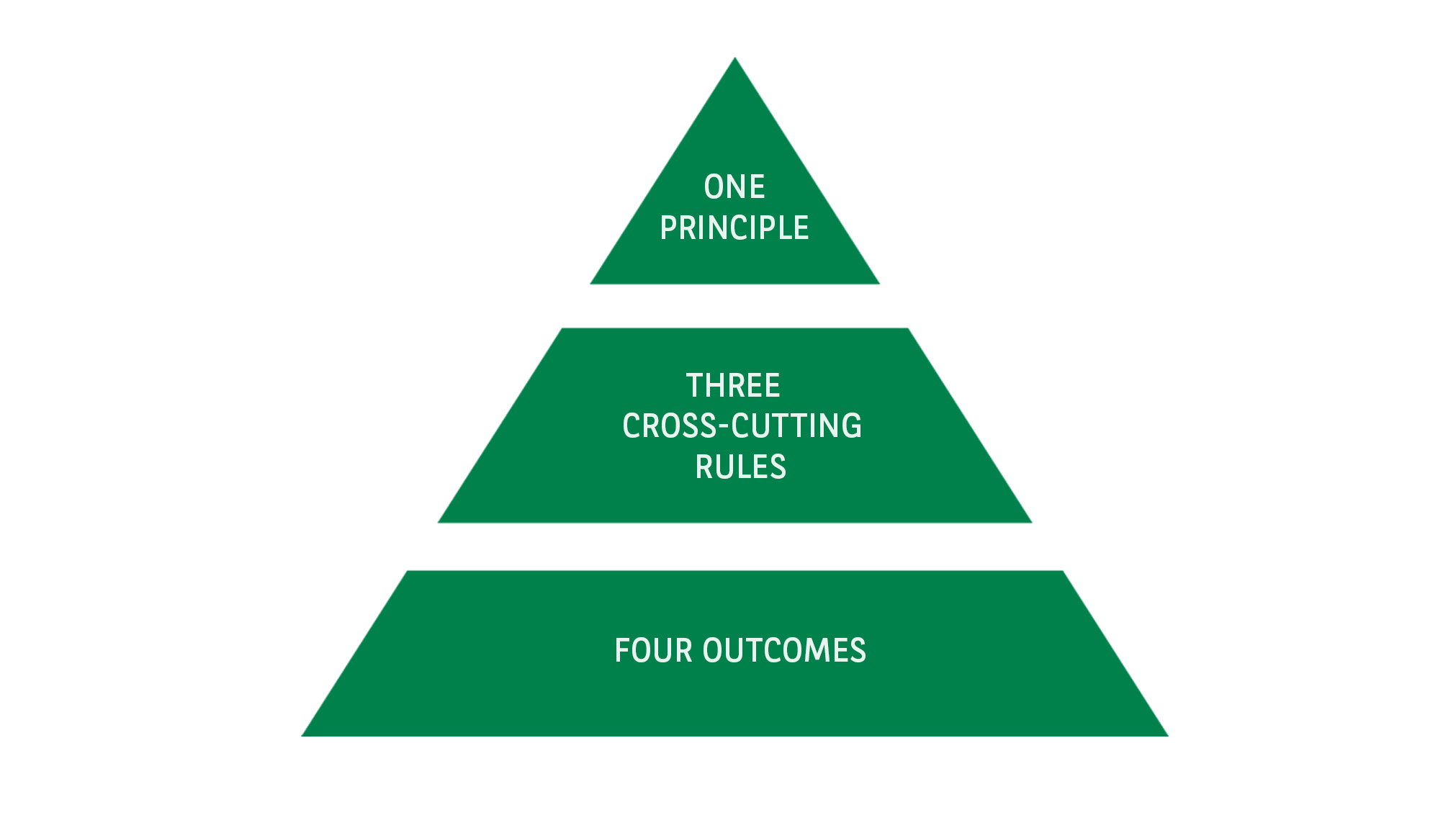

The FCA Consumer Duty

The FCA Consumer Duty requires firms to put their customers’ needs first.

-

-

- A new Consumer Principle that requires firms to act to deliver good outcomes for retail customers.

-

-

-

- Cross-cutting rules requiring firms to act in good faith, avoid causing foreseeable harm, and enable and support customers to pursue their financial objectives.

-

-

-

- Four Outcomes rules requiring firms to ensure consumers receive communications they can understand, products and services meet their needs and offer fair value, and the support they need.

-

What is expected?

The FCA has issued specific rules and guidance, the overarching expectations are that firms should:

-

-

- Put consumers at the heart of their business and focus on delivering good outcomes for customers.

-

-

-

- Provide products and services designed to meet customers’ needs, that provide fair value.

-

-

-

- Not seek to exploit customers’ behavioural biases, lack of knowledge or characteristics of vulnerability.

-

-

-

- Consistently consider the needs of their customers, at every stage of the product/service lifecycle.

-

-

-

- Continuously learn from their growing focus and awareness of real customer outcomes.

-

-

-

- Ensure that the interests of their customers are central to their culture.

-

-

-

- Monitor and review the outcomes their customers are experiencing and take action where needed.

-

-

-

- Ensure that their board or equivalent governing body takes full responsibility for ensuring that the Duty is properly embedded.

-

What does it mean for BNP Paribas Leasing Solutions?

We take the requirements of the Consumer Duty rules very seriously and have established a project team to ensure that we meet the deadlines set out for the implementation.

Under the language used by the FCA we identify ourselves as a “Manufacturer” of financial products.

As such we are currently conducting a review of all our products, their value, their target markets, distribution arrangements, monitoring and review process to ensure that they are in line with the requirements under the Duty.